1.1. Employers’ obligation to enter employees into the Automatic Enrollment System (AES)

Employers are obligated to enter employees in the Automatic Enrollment System (AES) pursuant to the provisions on automatic participation of the Individual Pension Savings and Investment System Law No. 4632, which entered into effect on January 1, 2017. Accordingly, employers deduct and send to the system 3 percent of the premium-based earnings and of the pension deduction-based salary for the private sector and the public sector, respectively. If the employee wishes to pay a contribution higher than this rate, he/she can request it from the employer. Employees have the right to stay in the AES for as long as they wish.

1.2. Employers Under the AES

As of January 1, 2019, you are obligated to include your employees in the AES by drawing up an AES contract with a pension company if you have more than five employees. If you have multiple workplaces, you must consider the total number of your employees in all of your workplaces. For company structures consisting of a combination of multiple independent companies, the number of employees can be evaluated individually or collectively for each company.

If you are a new employer and the number of employees declared in the first notification you need to submit to the Social Security Institution is five or more, you must include your employees in the pension plan from the first salary payment to be made from the beginning of the following calendar year.

If you started your operations before January 1, 2019, but the number of employees grew to five or more after this date for the first time, you must include your employees in the pension plan as of the first salary payment to be made at the beginning of the following calendar year when you notified the Social Security Institution that you have five or more employees.

If you are an employer that has included your employees in the AES pension plans, you must include your newly recruited employees in the pension plan by deducting the contribution from the first salary payment.

If your number of employees drops below five at a later date after joining the AES, you must continue to stay in the system and include new employees in the system.

1.3. Employees Required to be Included in the AES Plans

The AES applies to Turkish citizens and those who work as a salaried employee in the public or private sectors per Article 28 of Turkish Citizenship Law dated May 29, 2009 and numbered 5901 (employees that fall under Articles 4a and 4c of the Social Insurance and General Health Insurance Law No. 5510 and who participate in the funds established as per supplementary Article 20 of the Social Security Law No. 506).

As of the first day of the year on which they will be included in the system, you must include your employees who are under 45 years old automatically, and your employees who are over 45 years old upon their request.

The insured employees that fall under Article 5(g) of the Law No. 5510, for instance: the Turkish employees whom you put to work in a country with no social security agreement with Turkey, must not be included in the system.

1.4. Steps to be Taken for AES Inclusion

Step 1: Choosing the pension company

If you are an employer that falls under the AES, you are obligated to identify at least one pension company and enter into a contract with it for your employees. As part of the contract, your employees are entered into the system with the certificate issued in their names. It is up to the employee to decide on the funds for the contributions to be invested in. If the employee doesn’t choose, you will choose the relevant funds for the contributions. The system offers interest and non-interest fund choices.

When selecting a pension company, it is advisable to be informed about many aspects such as the pension company’s quality of service, technological resources, as well as the fund structure of the pension companies. This is because your employees’ preference of funds with or without interest is important. You, as the employer, cannot gain any advantages, including commissions, from the company due to the selection of company.

As an employer, you may receive services from private- or public-capital pension companies, regardless of whether you operate in the private or public sector.

You may change the pension company you receive services from. In other words, you may transfer your employees’ accounts from the current pension company into another one. If you were transferred to your current pension company from a previous pension company after remaining in the said previous pension company for at least two years as of the effective date of the contract you signed with the pension company you had chosen when you first entered the AES, you may transfer to other pension companies after at least one year from the transfer date.

Once you have decided on the pension company you want to transfer your contract to, you must contact the relevant company. Click to view the list of pension companies.

Step 2: Signing the pension contract

You must sign a contract with the pension company you have chosen to enter the AES. In this contract:

Annex A.6: Automatic Enrollment Group Contract and Employer Information Form of the Circular on the Individual Pension System provides information on the minimum requirements of the contract. Click to view the circular.

1.5. Your Obligations as an Employer

Setting authorized officials for the AES transactions: As an employer, you are required to establish your authorized department and officials to perform the AES-related transactions.

These authorized officials are responsible to fulfill your responsibilities as an employer in accordance with the AES and conveying your employees’ pension account-related requests to the pension company. Accordingly, they must carry out tasks, including selection of the pension company, signing a contract with the company, conducting all communication and information activities, calculation and payment of contributions, and informing the pension company about the employees’ requests for withdrawal from or leaving the system, suspension of contribution payments, changes in the fund distribution or type, or contribution amount, as well as other similar tasks.

In accordance with operational requirements, you may hand over all of these obligations as per the AES, except for selection of the pension company and deduction of the contributions, to the pension companies.

Selection of funds: As an employer, you are required to ask the employees to select a fund with or without interest, or make the selection for them, if they do not do so. Accordingly, in line with the fund preference, the contributions of your employees are invested in an interest-bearing or non-interest-bearing initial fund during the two-month initial period from the date on which they are notified that they are included in the pension plan.

Payment of contribution: You must deposit into the pension company’s bank account the deductions you make from your employees’ salaries at the latest on the business day following the salary payment date set forth by the contract you drew up with the pension company. The contributions that you transfer are invested in the pension mutual funds without being subject to any deduction and managed by expert portfolio managers. The distribution of the lump-sum amount you will send to your employees’ automatic participation accounts is calculated based on the information you will send to the pension company.

You, as the employer, are liable for the losses in your employees’ savings that arise from any incorrect information you send to the pension company. As the employer, you are liable for compensating the financial losses and costs in your employees’ savings that arise from the incomplete or late information you send to the pension company, or from your failure to send it, and for making the necessary corrections.

Meeting employee demands: Your employees cannot transfer their automatic participation certificates to another pension company. If you employ an individual who already holds an AES certificate and that employee makes a request, you can inform the employee that he/she can be included in the pension company with which your AES contracts are held by transfer, and direct them to the pension company.

After the initiation period is complete, your employees may request a contribution holiday. You are responsible for notifying the pension company of your employees’ requests for a contribution holiday.

Also, your employees may increase contributions above the legal minimum deduction rate (3 percent) by informing you, or decrease the increased rate, provided that the rate does not go below the deduction rate of 3 percent set forth by the Law No. 4632.

In addition, in the event that your employees who left the system by exercising their right of withdrawal request to be re-entered in the system, you must include your employee in the system by making a deduction from the second salary payment following the date of the request at the latest.

Inclusion of newly recruited employees in the AES :

| Is your workplace in the system? | Your new employee's age (*) | Your new employee's status in the AES | Required course of action |

|---|---|---|---|

| Yes | Under age 45 | Included in the AES at previous workplace and currently in the system | You must include your employee in the system again |

| Included in the AES at previous workplace but currently not in the system due to them leaving | You must include your employee in the system again | ||

| Over age 45 | Included in the AES at previous workplace and currently in the system | You must include your employee in the system again | |

| Included in the AES at previous workplace but currently not in the system due to them leaving | You must not automatically include your new employee in the system. However, you must re-include your employees in the system upon their request. | ||

| No |

Over and under age 45 |

Included in the AES at previous workplace and currently in the system |

Until your workplace is included in the AES, you will not need to do anything else for that employee. Your employee can make an individual payment for the automatic participation certificate opened at the previous workplace |

|

Included in the AES at previous workplace but currently not in the system due to them leaving |

Until your workplace is included in the AES, you will not need to do anything else for that employee. After your workplace is included in the AES, you must include employees under the age of 45 in the system automatically and employees over the age of 45 upon their request. |

(*) Whether the employees are over 45 years of age is determined based on the first day of the year on which they will be included in the system.

The Ministry of Labor and Social Security will impose an administrative fine for each breach of your obligations as per the AES. As the employer, you are also responsible for compensating any damages incurred by the employee due to an error on your end and covering all kinds of expenses related to unpaid, late or underpaid contributions.

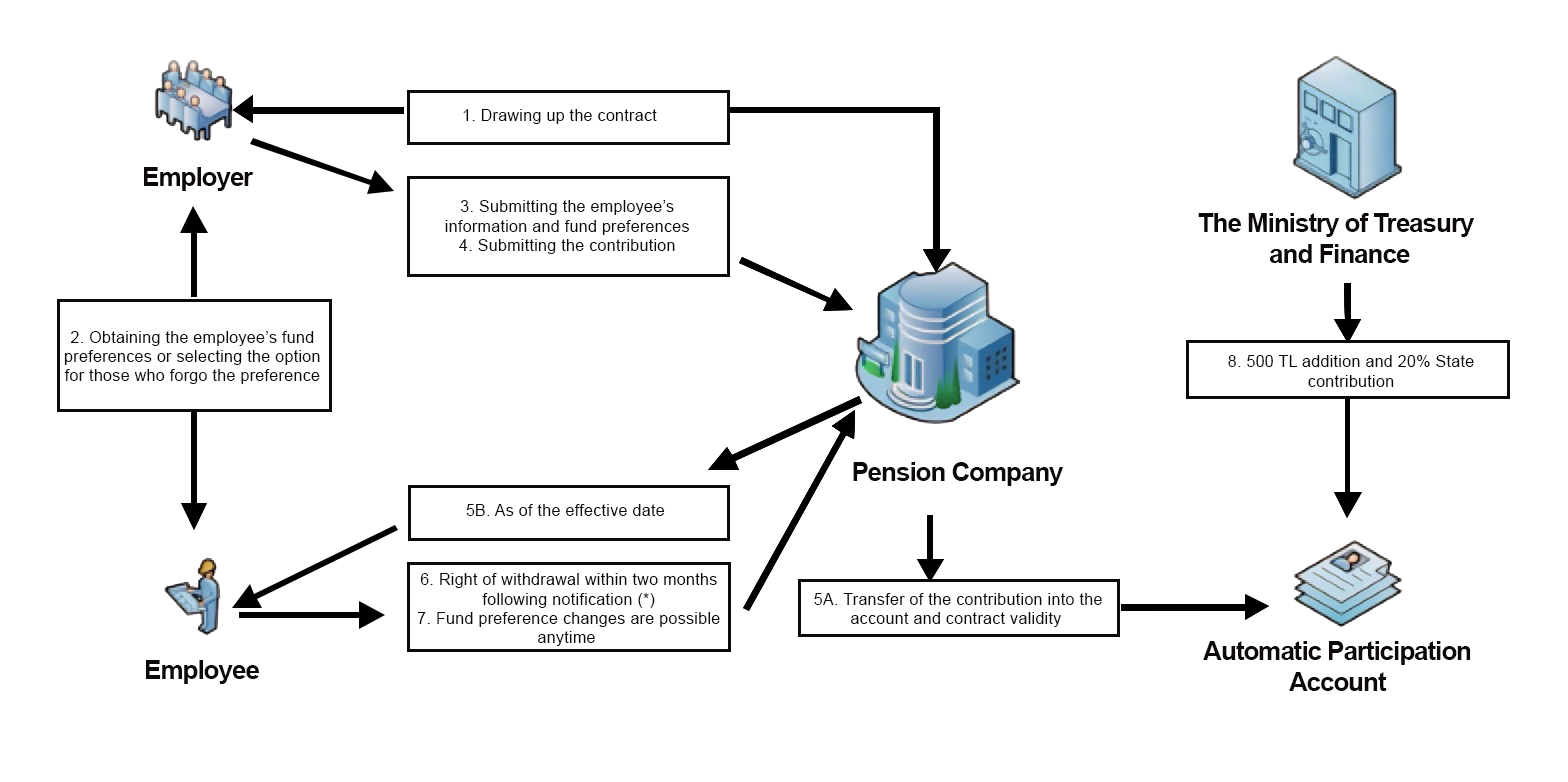

1.6. Functioning of the AES

(*)The employee can exercise his/her right of withdrawal in the initiation period, which is the first two months, and has the right to leave the system at any time afterwards. During the initiation period, contributions are guaranteed not to lose value.

Everything You Want to Know about the AES

Click for details on your employees’ rights and other matters in the Automatic Enrollment System.

1.7. Transfer of AES Contracts to Another Pension Company

For the transfer of the savings under contract with company A and the amounts in the state contribution account to company B, the contract must remain with company A for at least two years from the effective date, excluding those arranged with a transfer from another company. If your workplace’s contract with company A was also arranged by transfer, he/she must stay with company A for at least one year for the contract to be available for transfer again. In the transfers, this period is not sought separately for each participant or employee.

|

If you are an employer whose Auto Enrollment IPS account is with Pension Company A and you wish to transfer your savings to Pension Company B, you must perform the following procedures, respectively: |

|

|---|---|

|

1. You send the transfer request in writing or by electronic means to company A, the company with the IPS account. |

|

|

2. Upon receipt of the transfer request, company A sends the account statement, transfer information form, and request form to you by electronic means within five business days or makes it available to you from the secure area on the website. |

|

|

3. You apply to company B by mail or electronic means with the account statement, transfer information form and request form. |

|

|

4. If the transfer request is deemed appropriate, Company B proposes a plan to you and provides basic information on matters that may affect the transfer decision, particularly the deductions in the plan. You fill in the fields specified in the Transfer Request Form completely and submit the form to the pension company. |

|

|

5. In case you prefer the plan offered by company B, the automatic participation group contract drawn up for the transfer process is signed by you or approved by electronic means and sent to the relevant company. |

|

|

6. Company B starts the transfer process by registering the transfer information on the Digital Transfer Platform established by the PMC on the business day following the date of receipt of the request at the latest. |

|

|

7. Within the nine business days following the registration of the transfer information on the Digital Transfer Platform by company B, the savings of the requester and the amount in the state contribution account, if any exists, are transferred to company B by company A, and the contract enters into force on the date the savings are transferred. |

Note: The forms you will access from this page are examples of the forms in the Circular on the Individual Pension System and are provided for informational purposes only. For transfer transactions, you must obtain your documents from the relevant pension company.

The transfer is completed within 10 business days from the date on which the transfer documents are submitted to the relevant company by the employer.

2.1. Employers Motivating the Employees through Voluntary IPS Noncontributory Group Contract and Benefiting from Tax Advantages

You can enter your employees in the Individual Pension System (IPS) through noncontributory group contracts and encourage them to save for their future. This is an effective way to achieve employee motivation and foster company loyalty. The contributions paid on behalf of your employees can be recorded as expenses when calculating business income without associating them with the salary. Additionally, you can determine the vesting period, which is not to exceed seven years, for the savings arising from contributions paid for your employees and from their earnings.

The vesting period is the period specified in the contract for your employees to be entitled to all of the savings in their retirement certificate. This period cannot exceed seven years. In the event that your employee leaves employment or is removed from the non-contributory group contract, the pension company will make the payment to your employee according to the vesting period and rate decided by you. The employee may transfer the vested amount to another individual or group individual contract at another pension company, excluding the current or newly drawn up contracts as part of auto enrollment. The pension company pays you the unvested part of the savings saved in your employee’s account.

The minimum entitlement rates to be applied depending on the years are as follows:

Minimum Entitlement Rate by Contract Year (%)

| Which Year of the Contract Is Your Employee In? | ||||||||

|---|---|---|---|---|---|---|---|---|

| Duration Set Forth in the Contract for Your Employee to Qualify for All Savings (Year) | <1 | 1. | 2. | 3. | 4. | 5. | 6. | 7. |

| 0 | 100 | |||||||

| 1 | 0 | 100 | ||||||

| 2 | 0 | 0 | 100 | |||||

| 3 | 0 | 0 | 0 | 100 | ||||

| 4 | 0 | 0 | 0 | 75 | 100 | |||

| 5 | 0 | 0 | 0 | 60 | 80 | 100 | ||

| 6 | 0 | 0 | 0 | 60 | 70 | 80 | 100 | |

| 7 | 0 | 0 | 0 | 50 | 60 | 70 | 80 | 100 |

2.2. How do employers transfer voluntary IPS contracts to another pension company?

For the transfer of the noncontributory group contract with company A to company B, the contract must remain with company A for at least two years from the signing date, excluding those arranged with a transfer from another company. If your noncontributory group contract was arranged by transfer, the contract must stay with company A for at least one year for it to be available for transfer again. In the transfers, this period is not sought separately for each participant or employee.

|

If you are an employer whose Voluntary IPS account is with Pension Company A and you wish to transfer these savings to Pension Company B, you perform the following procedures, respectively: |

|

|---|---|

|

1. You send the transfer request in writing or by electronic means to company A, the company with the IPS account. |

|

|

2. Upon receipt of the transfer request, company A sends the account statement, transfer information form, and request form to you by electronic means within five business days or makes it available to you from the secure area on the website. |

|

|

3.You apply to company B by mail or electronic means with the account statement, transfer information form and request form. |

|

|

4. If the transfer request is deemed appropriate, Company B proposes a plan to you and provides basic information on matters that may affect the transfer decision, particularly the deductions in the plan. You fill in the fields specified in the Transfer Request Form completely and submit the form to the pension company. |

|

|

5. In case you prefer the plan offered by company B, the entrance information form and the pension contract proposal form prepared for the transfer process are signed by you or approved by electronic means, and sent to company B. |

|

|

6. Company B starts the transfer process by registering the transfer information on the Digital Transfer Platform established by the PMC on the business day following the date of receipt of the request at the latest. |

|

|

7. Within the nine business days following the registration of the transfer information on the Digital Transfer Platform by company B, the savings of the participant or the employee and the amount in the state contribution account, if any exists, are transferred to company B by company A, and the contract enters into force on the date the savings are transferred. |

Note: The forms you will access from this page are examples of the forms in the Circular on the Individual Pension System and are provided for informational purposes only. For transfer transactions, you must obtain your documents from the relevant pension company.

The transfer is completed within 10 business days from the date on which the transfer documents are submitted to the relevant company by the employer.