Calculation Method for the Funds Included in the Comparison Group

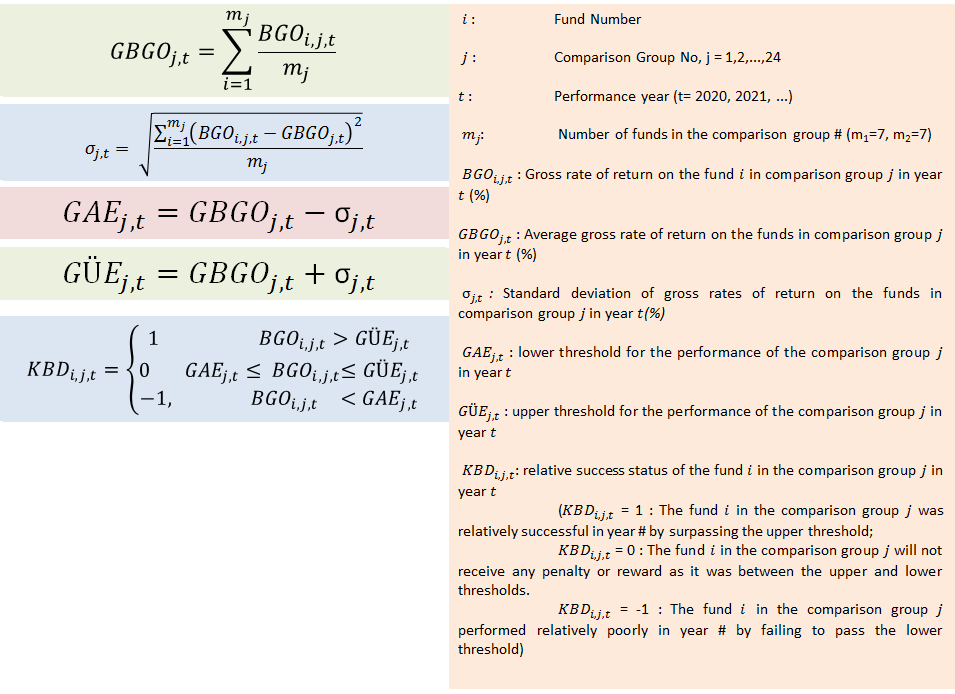

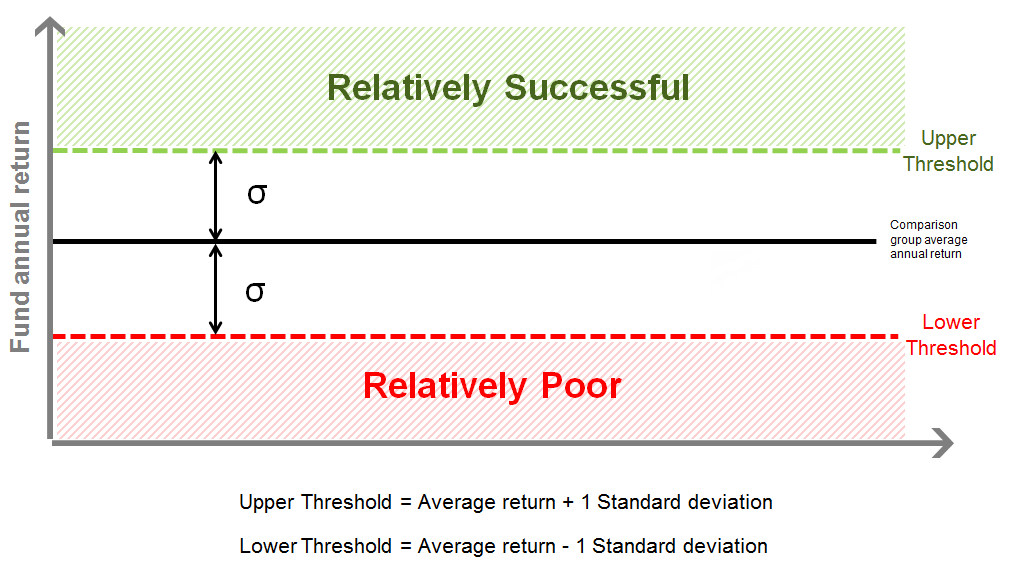

Values of “Simple average return rate - 1 standard deviation” and “Simple average return rate + 1 standard deviation” will be defined as lower and upper thresholds for each comparison group, and the performance of the funds with a gross return rate below the lower threshold will be considered “relatively poor,” and the performance of the funds with a gross return rate above the upper threshold will be considered “relatively successful.”

Note: Ratios such as Sortino or Sharpe are more effective in estimating risk-adjusted returns, however due to:

- the difficulty of creating a specific market for each comparison group;

- the difficulty of reaching an agreement as to which indices to assign how much weight;

- potential problems with the clarity of the method for stakeholders and the public;

- potential problems of creating a fixed market for the entire year in variable fund groups;

fund gross return rates, and comparison group simple return rates and standard deviations were used.

Calculation Method for the Funds Not Included in a Comparison Group

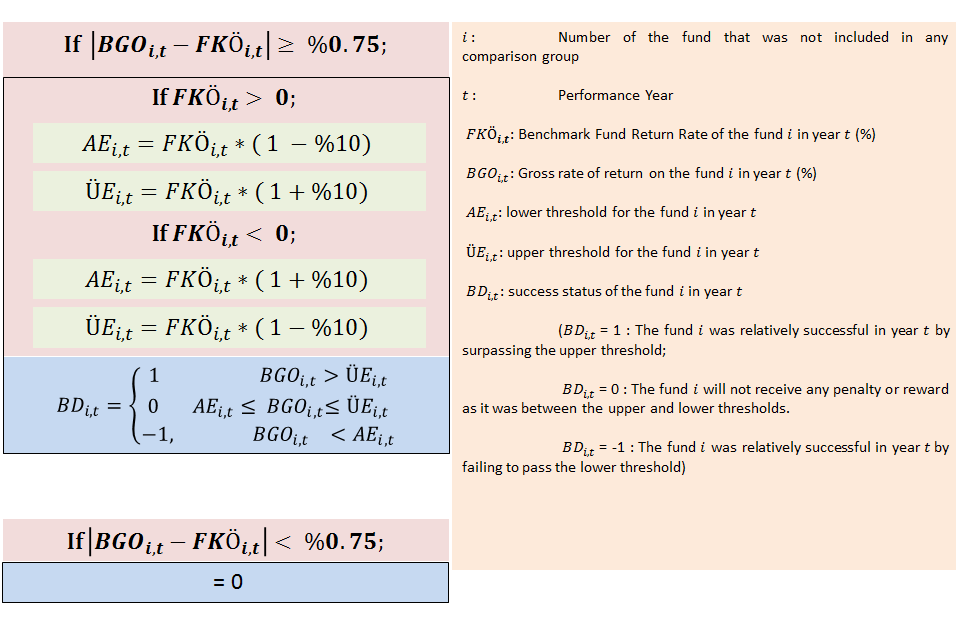

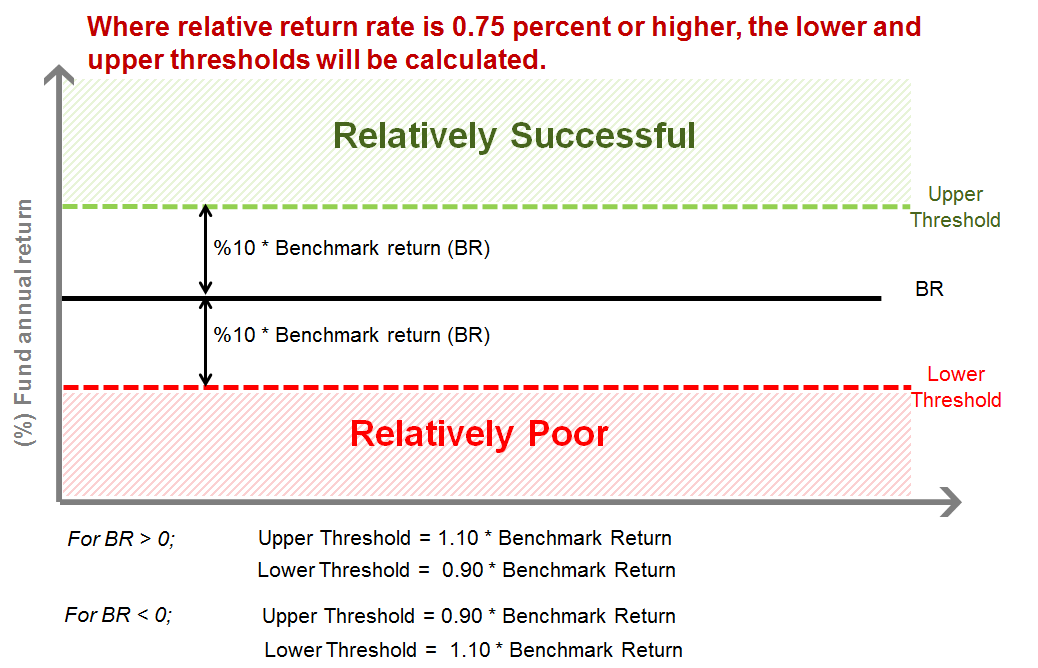

Each of the funds that are not included in a comparison group will be assessed by its own benchmark return, lower and upper thresholds will be “benchmark return * 0.90” and “benchmark return * 1.10” respectively, and if the difference between the gross return rate (%) and benchmark return rate (%) of the said funds is above 0.75 percent of the absolute value, penalties or rewards will be applicable.